Liquidity is Returning. Selection Remains Tight

The market is not reflating everything. It is selecting the assets the system needs.

This Week’s Read 30th May, 2026

Credit (HYG) moved higher away from the danger zone. We can now look toward a potential higher high. I explained the importance of HYG ETF here.

The dollar index, DXY, moved down slightly on the week. Again, helping to relieve pressure.

Copper remains robust and COPX copper miners look very promising.

TLT, the long bond ETF, gained on the week, as long bond yields continued to ease.

Gold was stable

Silver was down, 2.5%, on the week.

Ultimately, credit conditions stabilised while silver remain weak.

Weekly Interpretation

The markets have a chance to breathe once again. Capital allocation is being dispersed.

But this dispersal is narrow. Remember, this is central planning of a new economy build out.

It is not broad financial expansion of old. And that remains so important for people to understand.

The funding layer consists of assets connected to capacity, infrastucture, power, grid compute and collateral usefulness.

This is all part of the wider transition that I have been tracking for some time.

Yet, one of the most interesting signals is the divergence between energy.

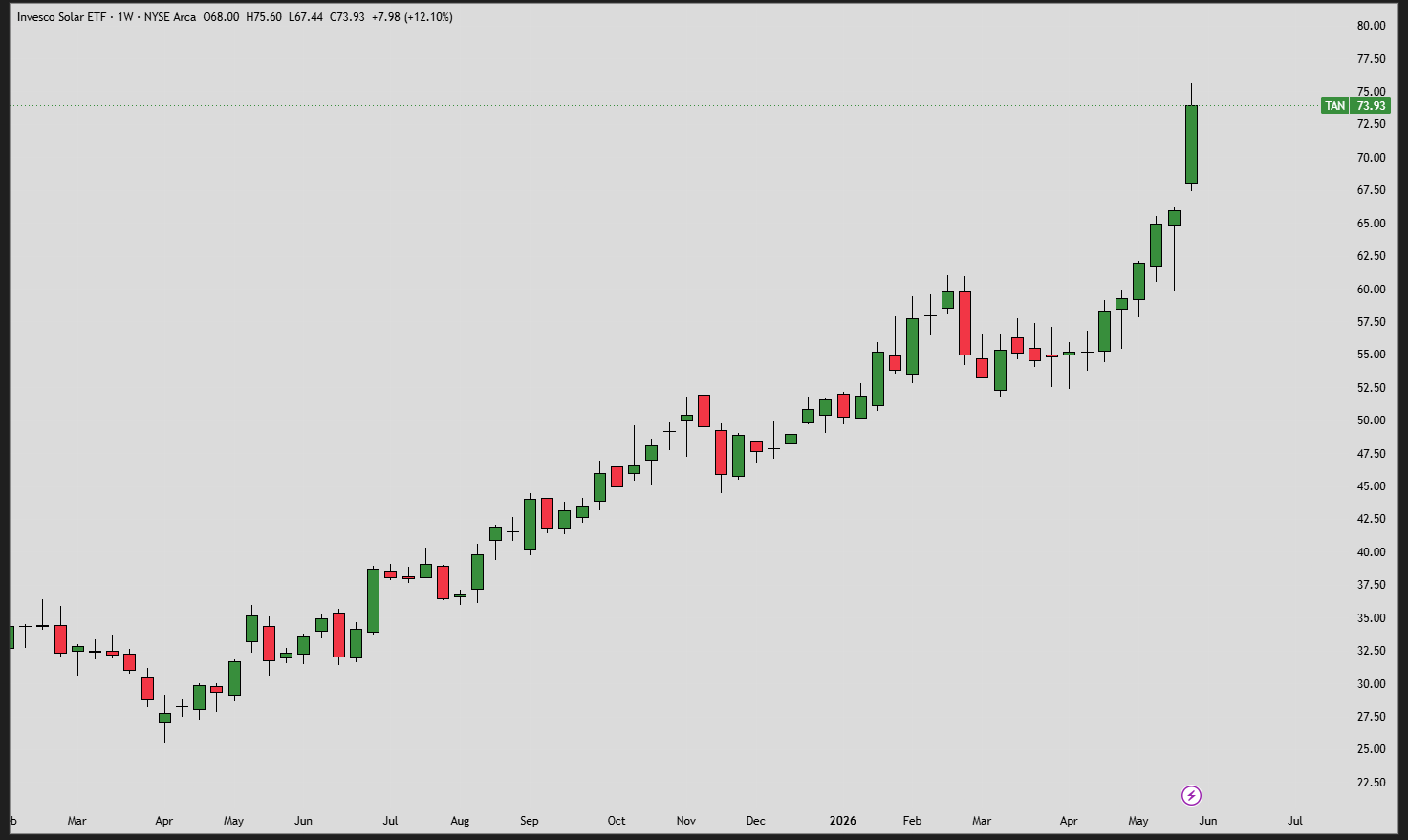

TAN Solar ETF was up 12% on the week:

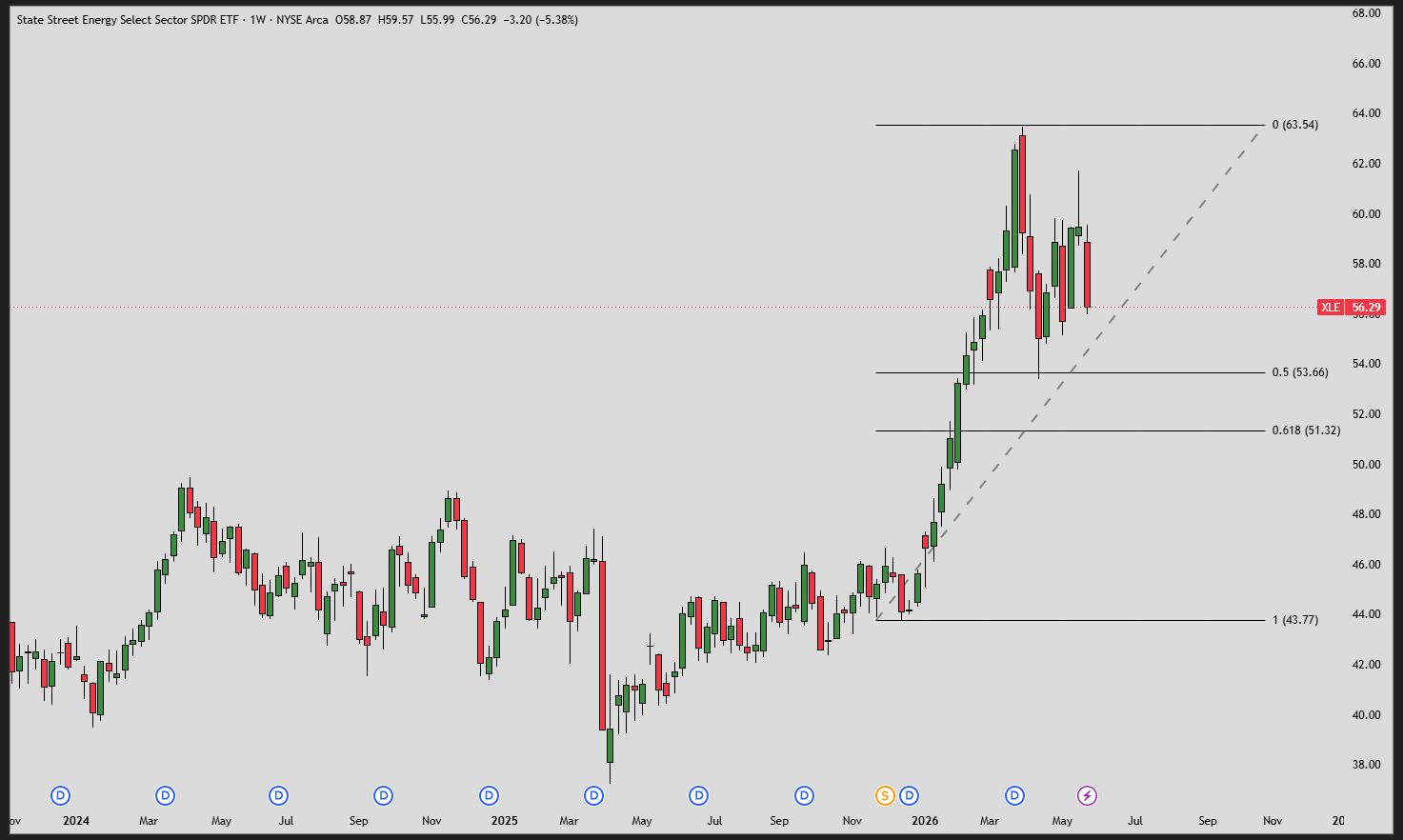

While traditional oil and gas is looking weaker represented here by XLE ETF:

AI requires collossal amounts of power.

Expanding the grid requires power.

Data centres require power.

And the new financial system requires vast physical capacity underneath it all.

But the key emphasis within these two charts is that credit is highly selective.

The Fed Has Changed the Rules

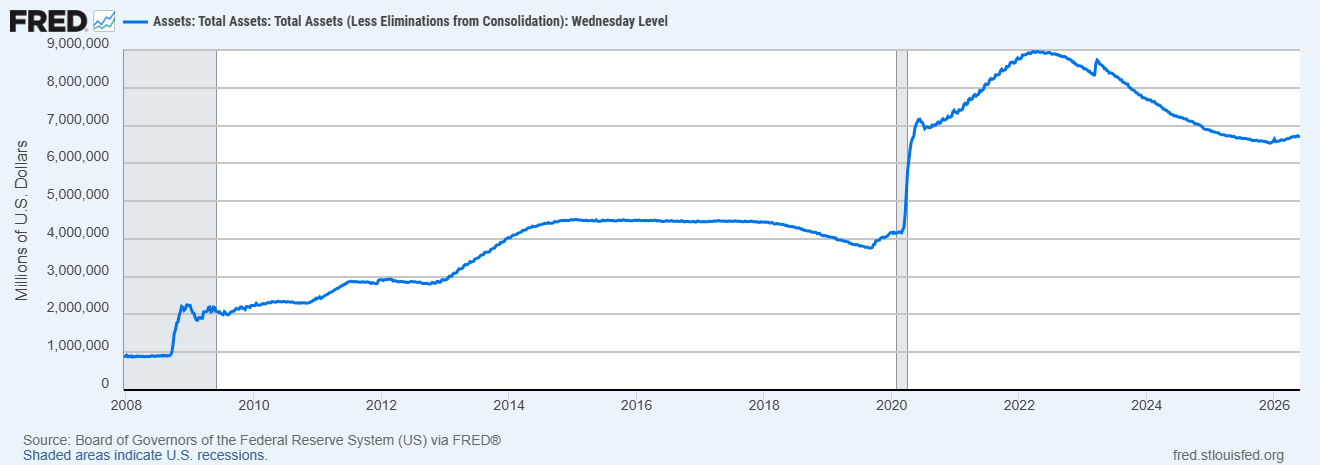

The post 2008 and post 2020 world, saw liquidity flow into financial assets almost indiscriminately. But the Fed’s interventions today are limited and selective.

The Fed’s recent interventions have been about short term liquidity injections. Unlike post ‘08 and post ‘2020 the Fed is not supporting long term bonds. It is not buying duration debt of 10,20 or 30 years. Only short term debt.

They are buying bills with newly created central bank money. That ensures the market stays liquid.

But it also caps rates on T-bills.

As T bill demand rises. Yields are stable and in line with the Fed Funds Rate - see above.

This stabilises credit by ensuring liquidity, but doesn’t really allow it’s expansion as long term borrowing is more expensive.

Therefore, equities become more selective.

The Fed is saying that cheap refinancing is long gone.

This is why we see such stress in markets that have long depended upon long term debt and easy refinancing.

The key point is that trust is shortening - From long bonds to T bills.

However, for gold holders, this emphasizes a key signal: