The Fed Steps Back, the Collateral Machine Steps Forward

Warsh continues Powell’s pivot from easy money to collateral control.

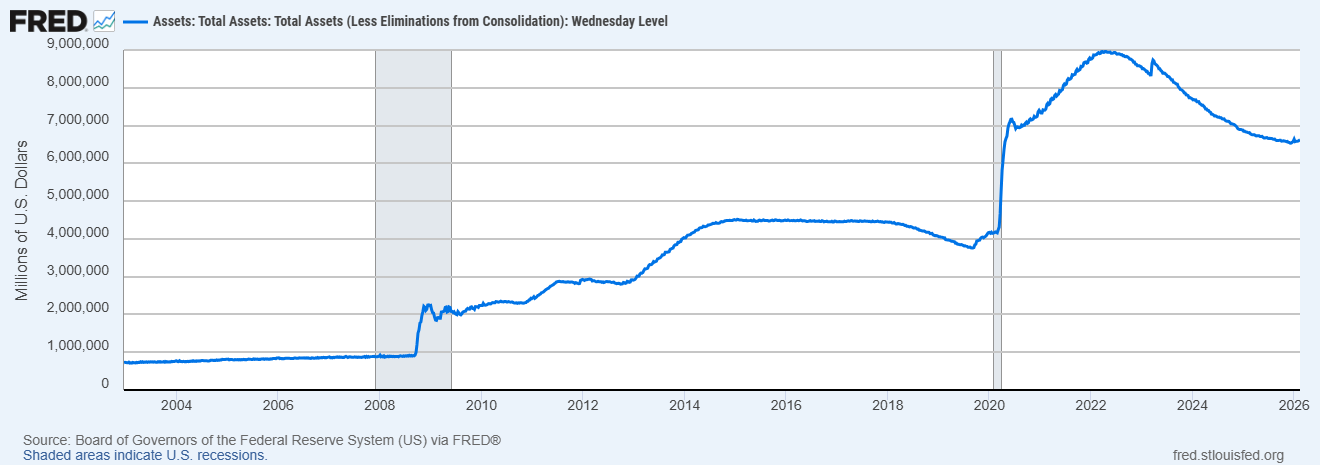

For years, the Federal Reserve and central banks more widely were the key instrument in providing continual liquidity to the markets. The old legacy financial regime was an increasingly central bank insulated model which helped suppress volatility and back-stop long-dated debt. When markets became unstable, liquidity support was often close at hand. The post 2022 pivot towards quantitative tightening (Fed balance sheet shrinkage), higher borrowing costs and more selective credit creation reflected a true step change toward a new financial architecture.

This new financial regime demands that there will be no more easy Fed hand-outs. It changes the terms on which liquidity is granted.

Following new Chairman Warsh’s recent presentation, some are opting to fade this current stance. I’d urge some caution because few appreciate the dramatic nature of the regime change underway.

I am not pay-walling this post because I think this regime shift is simply too important. If it helps you see the bigger picture, please like, restack, or share it. Yes, this feeds the algorithm gods - but more importantly, it helps get the signal to people before the noise overwhelms it.

What is really happening is that central banks throughout major nations are stepping back from their old ways of financial engineering while government treasuries move toward liquefying and mobilizing the entire nation’s asset base.

I just want to reinforce this point: the Fed and other global central banks will try to avoid printing money to monetize public debt and protect long-dated sovereign bonds. Policy bias has shifted away from broad support. Instead, private wealth will be mobilized. That is dangerous for the general household.

Warsh’s Fed follows the post 2022 pivot set by Powell to move us toward this new collateral based financial system.

The rate decision was actually of little real interest. What was more meaningful was the removal of forward guidance. Warsh stating that forward guidance is “not well suited to the current policy conjuncture.” Originally, forward guidance was implemented to improve clarity but it really served as a liquidity tool which allowed markets to borrow against Fed future promises. Warsh then went on to reinforce the perspective that markets should respond to data and not mirror Fed conduct. In essence, he was emphasizing that central-bank language had become a form of credit permission. Prior to 2022, that permission was easily granted but it is now uncertain.

Of course, the new system means that credit is not granted against promises or reassurances. Instead, new purchasing power will be granted against collateral, verified cash flows and real time information.

Liquidity is becoming conditional. The incentives all align:

The Fed wants discipline, real-time data and less focus upon their direct role

The Treasury needs sustained demand for short term government debt

Wall St gets to provide the machinery to turn more assets into programmable liquidity.

I have listened to a number of commentators who have supported the stance of abandoning easy liquidity. Yet, none have considered the big picture and the intended destination of the financial system.

To me, it is simply a case of meet the new boss; the same as the old boss. The new system looks more disciplined, than the old. The old boss was central bank liquidity. The new boss is collateral eligibility, tokenized claims and real-time enforceability.

Volatility Becomes the New Market Discipline

The old system considered volatility to be a major problem. A system centred around trust and promises will always function better in smoother market conditions where promises can be easily maintained.

Yet, in the transition toward a new financial regime, volatility becomes incredibly useful for the following reasons:

Volatility discourages excessive leverage (debt enhanced positions)

Refinancing becomes more dependent upon verified cash flow and acceptable collateral

It increases longer term borrowing costs

It punishes the old carry trade model of using low rates to speculate

It also forces market participants towards hold short term T-bills and other high-quality collateral.

Volatility means that no central bank needs to say: “we’re banning excessive borrowing.” Instead, weak borrowers are forced to discipline themselves.

This makes bad borrowing scarce. Think Yen carry trade, long-dated sovereign debt and private credit as clear examples.

The flip side is that liquidity may become more available for assets that the system can verify - enter tokenization.

The market reaction to Warsh’s release was predictably; volatility.

But Trump Wants Lower Rates

True enough. But if central banks become more disciplined and avoid excessive balance sheet abuse (via QE or money printing), while at the same time imposing more treasury collateral plumbing; it can restore confidence in central bank discipline. Then later rate cuts could coexist with a better collateral framework.

Remember, it will mean that new money is only created against verified, pledged collateral. Very different from the excesses of the prior regime. Warsh can then be held up as a paragon of virtue. All the while, households pledge their assets into institutional custody, tokenized products and collateralized lending structures.

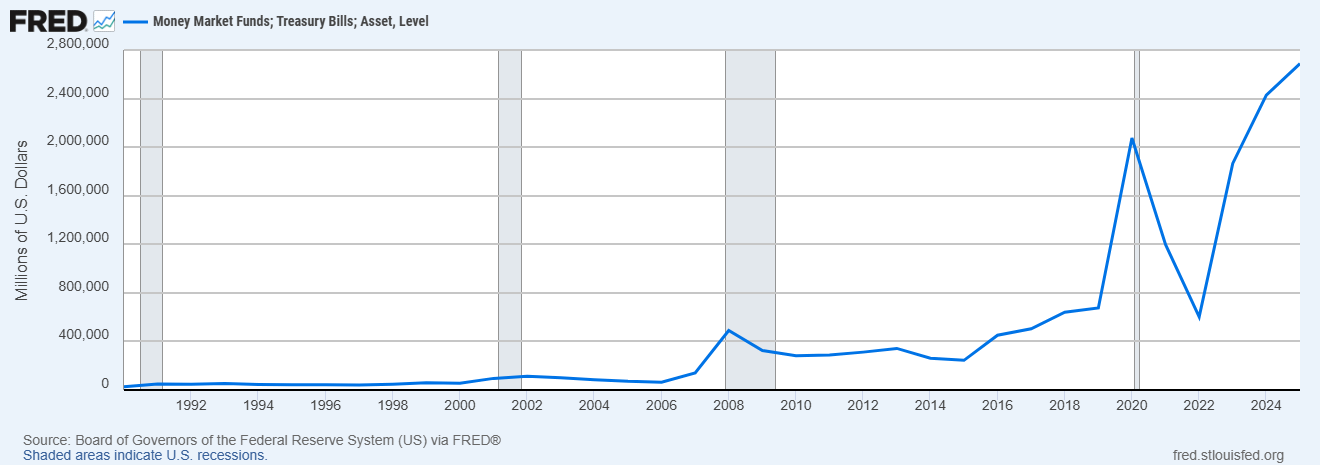

Nevertheless, as monetary trust is, in time, restored, a collateral backed system seems likely to create persistent demand for T-bills, particularly from money market funds (see chart below), stable coin issuers and tokenized treasury providers. So demand will certainly support the front end of the yield curve. Yet issuance will remain heavy.

But in that environment low rates won’t necessarily mean easy credit. Instead, low rates will be permitted for acceptable collateral.

Reinforcing Demand for T-Bills

I keep emphasizing the point that long duration debt is being punished. Yet, short term sovereign debt is planned to become the centre of economic gravity in the new system. If the Fed retreats from being the main engine of market liquidity, a void needs to be filled. Treasury collateral is the obvious candidate.

T-bills are short dated promises, widely accepted, highly liquid and state-backed. Money market funds, stable coin providers together with banking regulations and newly high speed tokenized versions are reinforcing demand for these assets which are considered top tier collateral.

That makes T-bills the raw material of global dollar liquidity.

The chain looks like this:

T-bill issuance → stable coin reserves → tokenised Treasuries → digital collateral → programmable settlement.

This means that the Treasuries role shifts to being the supplier of base collateral for the next financial system. Government debt growth becomes a necessity to help sustain the monetary system as the Fed relieves itself of the need for continual QE.

Yet, over time, this extreme financial alchemy means that the collateral layer (short term debt) becomes the risk vector as demand fuels the need for ever greater sovereign debt burdens.

The risk, seemingly baked into the cake, is that the system replaces one dependency for another. The Fed no longer supports long term debt and becomes dependent upon short term debt. This makes the system highly sensitive toward any funding market stress.

A New Focus - For Wealth Preservation

My interpretation of Warsh’s statement, in the context of financial regime change, is that it means that our focus should evolve.

As the Fed’s steps back into the shadows, we need to shift our perspective away from a simple “what will the Fed do next” perspective toward a more structural question:

Which assets will the new system recognise as liquidity bearing collateral?

For households across major nations, the danger goes beyond owning the wrong asset. The greatest risk is being forced to act and having to pledge the right asset, such as a home, on bad terms. Reducing dependence upon continual refinancing is a must.

Yet, the key collateral beyond short-dated sovereign debt will very likely extend to the following:

Verified hard assets;

Productive infrastructure;

Strategic commodities;

Settlement and custody rails;

Assets with durable cash flows.

While at the same time we can expect the following assets to feel the heat of far tighter credit permission:

Long-duration speculation;

Weak private credit;

Overleveraged property;

Zombie companies;

Unprofitable growth equities - that do not receive strategic support;

Assets dependent on cheap refinancing.

Ultimately, the core market implication is simple:

Price will become an increasing function of liquidity and liquidity will be downstream of collateral status

Warsh is implicitly emphasizing the transition toward an asset selection regime. Assets that attain collateral status receive a premium. Assets that lose easy refinancing access get discounted.

Credit is becoming harder and more permissioned and that means everyone should be reducing their reliance upon ease of debt roll-over.

Signals to Watch

To test and track this transition, we will be closely tracking the following signals in our ongoing posts:

T-bill issuance share;

Stable coin reserve composition;

Growth in tokenised Treasury assets;

Repo and SOFR stress;

Treasury auction tails;

HYG and LQD credit spreads;

Private credit markdowns;

Collateral eligibility rule changes;

Gold versus real yields.

Yet, by far and away the biggest signal is if we continue to see support for short duration sovereign debt while speculative credit faces stress.

That tells us that liquidity is not disappearing, it is simply being redirected.

Of course, we’ll be carefully tracking the assets that are attaining liquidity status, alongside those which are losing their refinancing privilege while identifying where we should be paying attention before it becomes obvious.

I am not pay-walling this post because I think this regime shift is simply too important. If it helped you see the bigger picture, please like, restack, or share it. Yes, this feeds the algorithm gods - but more importantly, it helps get the signal to people before the noise overwhelms it.

Thanks much for this analysis and not for it to be behind a paywall; this is very pertinent

Brilliant peice again, Thankyou Miles for your insight.